The LLM Wars: Who's Winning the Battle for Your Brain?

Three tech titans walked into an AI race. One had a two-year head start. One had a search monopoly. One had the best product. The winner isn’t who you’d expect — and the race is far from over.

The consumer AI market has consolidated with unusual speed. In an industry famous for fragmentation, ChatGPT, Google Gemini, and Anthropic’s Claude have emerged as the three serious contenders for the same prize: the place people go to think. Understanding who’s actually winning requires looking past the headlines and into the mechanics of how people adopt and abandon these tools.

The Incumbent: ChatGPT’s Brand Tax

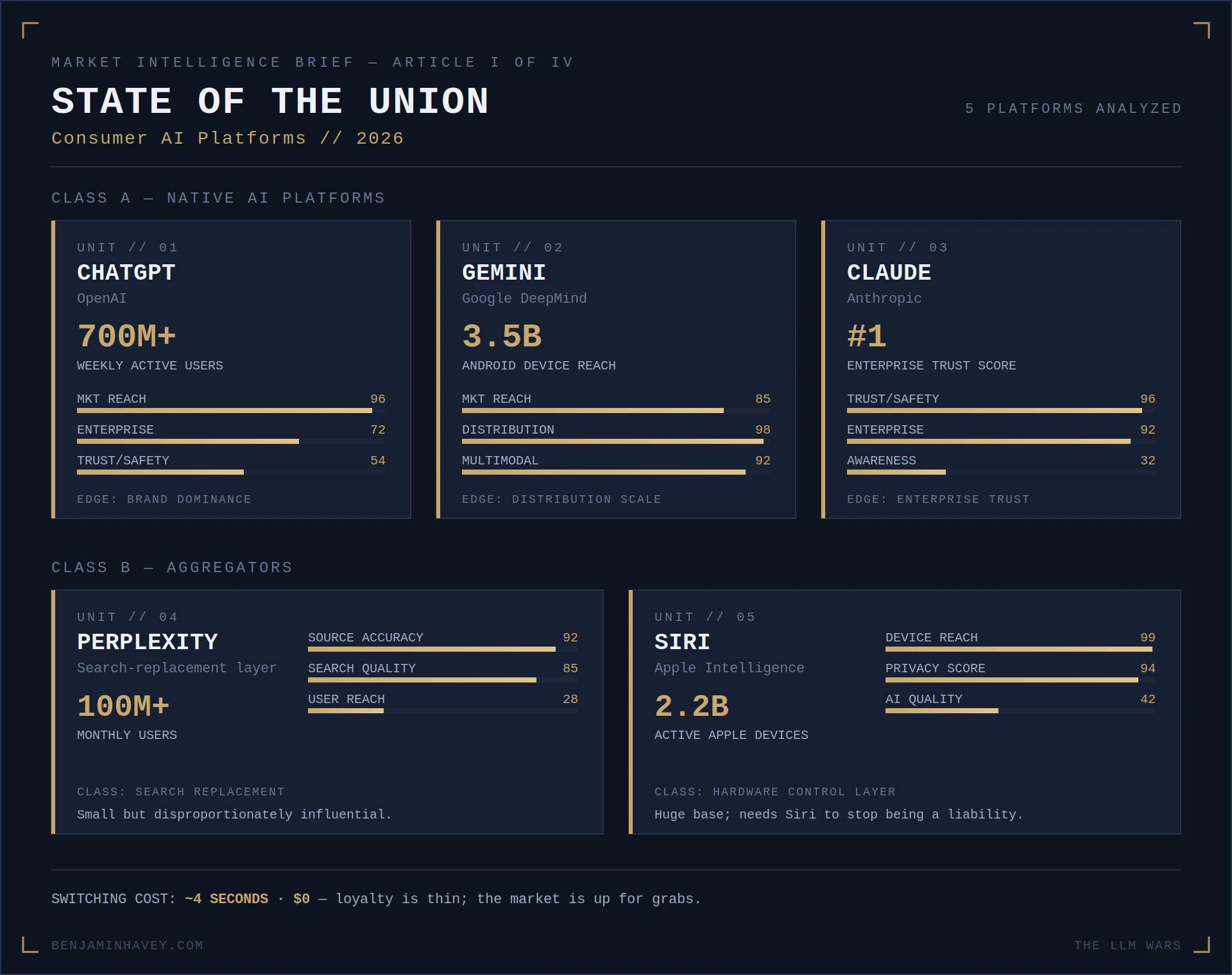

OpenAI got there first, and the numbers show it. ChatGPT commands somewhere north of 700 million weekly active users as of early 2026. More meaningfully, it has achieved something almost no software product ever does: it became a verb. “I’ll just ChatGPT it” has entered the cultural lexicon in the same way “Google it” did two decades ago.

But genericization is a double-edged sword. Users who say they “use ChatGPT” are often describing a behavior — querying an AI — more than a loyalty. Brand dominance without product dominance is a precarious position, and OpenAI knows it. The company has been sprinting to maintain its lead through rapid model releases, multimodal capabilities, and a consumer app that keeps improving. The question is whether being first will keep being enough.

The Distribution Machine: Gemini’s Hidden Advantage

Google’s Gemini may be the most strategically interesting player in this market — not because it’s the best model, but because it doesn’t need to be.

Android runs on roughly 3.5 billion active devices worldwide. Google Search processes over 8 billion queries a day. Google Workspace sits in the productivity stack of hundreds of millions of professionals. Gemini is threaded through all of it. When your AI is the default on the world’s most-used phone and the world’s most-used search engine, you don’t need to win on quality; you need to not lose on it.

Google’s existential challenge here is that its advertising-driven business model has structural tension with AI that answers questions directly. But make no mistake: in the long game of AI adoption, distribution beats product until product becomes dramatically better. Google is betting it can close the quality gap before the market consolidates around a competitor.

The Dark Horse: Claude’s Professional Credibility

Anthropic’s Claude doesn’t lead in consumer awareness. It leads in something harder to measure and more valuable to certain audiences: trust.

Claude has quietly become the model of choice among professionals, researchers, and enterprise users who need an AI that’s less likely to hallucinate with confidence, more likely to say “I don’t know,” and built with safety architecture that can survive a procurement audit. It’s the AI that lawyers, doctors, and executives recommend to each other in the ways people used to recommend a reliable accountant.

Consumer recognition remains Claude’s gap. Ask a random person on the street to name an AI chatbot and you’ll hear ChatGPT. Ask the average senior knowledge worker which they actually trust for high-stakes work, and Claude shows up disproportionately in the answer. The challenge — and opportunity — is translating that professional credibility into broader consumer awareness before the window closes.

The Aggregators: A Different Game Entirely

Two other names belong in this conversation, though they’re playing a fundamentally different game.

Siri and Apple Intelligence represent perhaps the most tantalizing wildcard in consumer AI. Apple’s hardware install base is enormous — over 2.2 billion active Apple devices globally — and its users skew toward exactly the demographic that early AI adoption is concentrated in. But Siri has spent a decade as the punchline of voice-assistant jokes. Apple Intelligence, which routes queries through third-party models including OpenAI’s, is less an AI strategy than an AI aggregation strategy. Apple is betting that controlling the hardware and the interface matters more than controlling the model. They may be right, but they need Siri to stop being a liability first.

Perplexity is the most interesting small player in the space. Growing fast among researchers, journalists, and professionals who’ve quietly begun replacing Google with it for research queries, Perplexity is less a chatbot than a search engine that actually reads things for you. It cites sources, synthesizes information, and bypasses the ten blue links that nobody clicks anymore. Its user base is small relative to the giants, but it’s disproportionately influential and disproportionately satisfied.

Here’s how the landscape breaks down at a glance:

What Actually Drives Switching

Here’s the uncomfortable truth for all of these companies: user loyalty in AI is thin. The switching cost of moving from ChatGPT to Claude is approximately four seconds and zero dollars. What drives adoption and retention in this market isn’t contracts or ecosystems — it’s Tuesday.

When a model gives you a bad answer on a task you care about, you try the next one. When that one is better, you stay for a while. The market is still in an exploratory phase where users are building mental models of which tool is best for which job. That fluidity makes this one of the most contested consumer markets in tech history — and one where the leaders are never entirely safe.

The Outlook

No one has won the LLM wars yet. The next twelve months will be shaped by a few key variables: whether any company can build enough switching costs to retain users through a bad product cycle, whether enterprise contracts consolidate around one or two providers, and whether Apple can finally make Siri relevant before one of the three main contenders locks up its user base.

The market is real, enormous, and up for grabs. Place your bets accordingly.

This is Part 1 of a 4-part series on the State of the Union in AI. Part 2 covers the image generation market.